What is the Corporate Sustainability Reporting Directive (CSRD) and its goals?

The CSRD is an EU Directive that amends the Non-Financial Reporting Directive’s scope and reporting requirements (NFRD). While the NFRD provided guidelines for ESG reporting, the CSRD will introduce mandatory reporting standards – including detailed environmental and social impact reports – that allow stakeholders such as investors and policymakers to better understand and evaluate a company.

The Corporate Sustainability Reporting Directive marks a transformative era for companies within the EU and beyond.

Key requirements of CSRD

The CSRD introduces several critical requirements that organizations must adhere to in their sustainability reporting. These standards ensure transparency, comparability and accountability and push companies to integrate sustainability into their operations, from top to bottom.

Disclosure formats and integration

Digital accessibility and integration

Disclosures must be integrated into the company’s Management Report in a digitally accessible format, adhering to the European Single Electronic Format (ESEF) regulation.

Standardized digital submission

Sustainability data must be submitted in a standardized digital format, enhancing the ease of checking and comparison within the European single access point database.

Scope and reporting timeline

The CSRD mandates comprehensive sustainability reporting for a broad range of entities, both inside and outside the EU.

The first reports are due in 2025 for large companies, covering the fiscal year 2024.

Timelines extend to 2029 for various entities, including non-European companies with EU branches or subsidiaries.

Comprehensive reporting requirements

Report coverage

Reports must cover environmental protection, social responsibility, human rights, anti-corruption, bribery, and diversity on company boards.

Reporting must follow the double materiality concept (see below), detailing how companies affect and are affected by environmental and social issues.

Enhanced credibility through auditing

Limited assurance auditing

The proposed limited assurance audit requirement at the program start aims to enhance the credibility of the data submitted, ensuring the information is reliable and verifiable.

Reasonable assurance audits are likely to be required in the future.

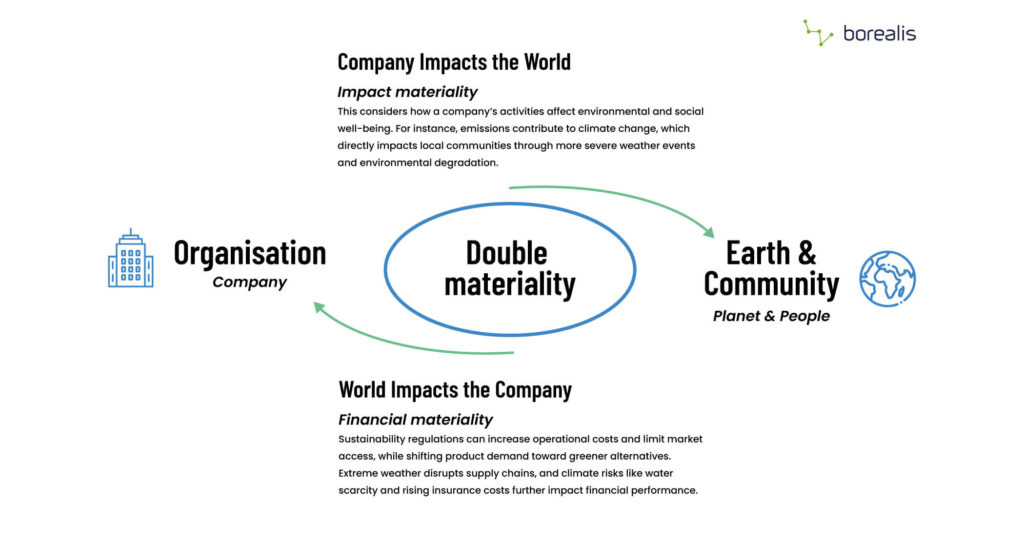

The double materiality requirement: A 360-degree view of your business

Companies must consider how their actions impact both people and the planet and how sustainability issues can affect the company’s financial well-being.

Double materiality acknowledges risks and opportunities from both financial and non–financial perspectives.

Impact materiality considers the consequences of a company’s activities on external stakeholders, including society and the environment. According to the European Sustainability Reporting Standards (ESRS), a sustainability topic is material from an impact perspective if it has significant actual or potential positive or negative influences over short-, medium-, and long-term time frames. Impact materiality includes impacts across the company’s operations, plus their upstream and downstream value chains.

Financial materiality focuses on sustainability matters that could influence a company’s economic performance. This aspect assesses risks and opportunities that may affect the company’s cash flows, cost of capital (i.e. the expense incurred by a company to fund its operations and investments), access to financing, and overall financial health. Financial materiality is vital for providing relevant information to investors, lenders, the media, etc.

What’s involved in a double materiality assessment?

Double materiality requires businesses to evaluate and report on sustainability matters from both an impact and a financial perspective. This double approach ensures comprehensive transparency and accountability.

These assessments should:

- Utilize stakeholder engagement to understand stakeholder concerns and priorities

- Use quantitative and qualitative data insights to assess the significance of sustainability issues.

- Evaluate impacts and financial effects over short-, medium- and long-term timeframes to capture a complete picture of risks and opportunities.

Disclosures and reporting

Once material matters are identified, companies must disclose the processes and outcomes of their materiality assessments. Companies will be expected to format these disclosures according to the European Sustainability Reporting Standards (ESRS).

Integration with business strategy

The findings from double materiality assessments are designed to inform the company’s business strategy and decision-making processes.

Companies in the EU won’t be the only ones affected …

EU officials estimate that more than 50,000 European companies will have to report, and according to recent research from Refinitiv, so will nearly 10,400 foreign companies that have an EU stock listing, as well as more than 100 companies that aren’t listed in the EU but have more than €150 million in local revenue.

Of the total number of companies identified, 31% are US-based, 13% are Canadian, and 11% are from the UK.

Scope and reporting timeline

Foreign companies required to report include:

- Companies that have listed securities, such as stocks or bonds, on a regulated market in the EU

- Companies that have annual EU revenue of more than €150 million and an EU branch with net revenue of more than €40 million

- Companies with an EU subsidiary that is a large company, defined as meeting at least two of the following three criteria:

- More than 250 EU-based employees

- A balance sheet above €20 million OR

- Local revenue of more than €40 million

Enforcement, compliance and penalties

Slated sanctions for non-compliance will be significant, ranging from monetary penalties to incarceration.

Regulators in individual EU countries will be responsible for enforcing CSRD compliance, meaning that procedures and penalties could look very different across various jurisdictions.

Consequences for non-compliance

Civil and criminal liability

Companies and their leaders may face fines, financial sanctions, and even imprisonment for failing to meet the reporting requirements or for providing incomplete or misleading information in their sustainability reports.

Reputational damage

Publication of non-compliance investigations/or decisions could create reputational harm and affect a company’s relationships with investors, customers, employees, and other stakeholders.

Investor scrutiny

Investors and stakeholders will no doubt increasingly scrutinize companies that fail to comply with the CSRD, which could lead to protests or boycotts, decreased share prices, or even divestment.

Capitalize on this transformational opportunity!

Complying with CSRD is an extraordinary opportunity to showcase your company’s commitment to sustainability, differentiate your brand, future-proof your business model and catapult past competitors.

In a world of environmental challenges and shifting societal standards, resilience is key.

Embrace the CSRD and boost company resilience and reputation, plus attract new business, investments, talent and customers!

For over 20 years, Borealis powerful software has helped more than 500 clients improve their stakeholder data management. Talk to one of our experts.

The Borealis application strengthened our social programs, providing us with a tool to demonstrate transparency in our consultation, communication and eligibility processes in the social area. It also provides an integrated monitoring system of environmental quality.

Ezio Buselli Canep,

VP Environment, Health and Safety at Chinalco

The Borealis application’s analytics and report features have been extremely important for our reporting requirements to senior management and lenders. The system as a whole has been the backbone of our social performance institutional memory that allows to show effective compliance with lender performance standard requirements.

Ben Chapman,

Site Manager at Monkey Forest Consulting

To me, the main benefit of Borealis is that it gives us a central repository where anybody from the various lines of business – whether that’s Environment, Project Delivery, Indigenous Relations, Community Relations – can go in and see exactly what consultation work has been done: who we’ve been consulting with, what are the outcomes of that, and then pull reports from the same source.

Paul Dalmazzi,

Environmental Planner, Hydro One

I am a strong supporter of the Borealis software. As a technological tool, it gives us everything we need to efficiently manage our ESG program. As Feronia overcomes its infrastructural and organizational challenges, the value we receive from this tool will only grow.

Xavier Dexarniere,

CEO, Feronia

So far, everyone I’ve shown this tool to who are not part of our organisation – other consultants or customers – have been impressed by the way Government Affairs (GA) can be organised. We look forward to ongoing improvements that will help us perfect our work.

Regional Government Affairs Lead, Zuellig Pharma

How Borealis can help your company with CSRD compliance

Our CSRD software offers fully–integrated modules to simplify your company’s everyday operations and CSRD compliance tasks, including stakeholder outreach and engagement, data capture, analysis and insights, reporting and verification.

Data collection & management: Build a solid foundation for effortless reporting

This stage is crucial. You’ll want to ensure you can easily gather all the information you need for your CSRD report, including data on environmental impacts, social responsibility, and governance practices. Borealis CSRD management software captures your information in real–time in a single source of truth, ensuring your reports are up to date.

Real-time data capture

- Borealis CSRD monitoring software tracks engagements, impacts, initiatives, and practices in real time.

- Enables comprehensive logging of stakeholder interactions.

API integration with other systems

- Our API integrates with tools like Power BI and Enablon for centralized data collection

Double materiality assessment: Don’t miss a beat!

Identifying the sustainability issues that matter most to your company and stakeholders (financial, social and environmental) is key. Borealis CSRD software streamlines this process, helping you prioritize these aspects and ensure your assessment meets ESRS requirements.

Materiality assessments

- Borealis CSRD management software allows you to prioritize sustainability issues (financial, social and environmental impact).

- Creates a comprehensive assessment that meets ESRS requirements.

Stakeholder engagement

- Our API integrates with tools like Power BI and Enablon for centralized data collection

Reporting & disclosure: Present a clear picture

Creating a comprehensive CSRD report that details your company’s sustainability performance according to ESRS guidelines is vital. Borealis CSRD reporting software simplifies this stage by ensuring your report covers all required disclosures (climate, biodiversity, water and social impacts) and effectively communicates your commitment to sustainability.

Structured reports

- Illustrates compliance with ESRS guidelines.

- Provides comprehensive disclosures on governance, strategy and risk management.

Compliance documentation

- Includes all required disclosures (climate, biodiversity, water and social impacts).

- Efficient tracking of ESRS compliance.

Continuous monitoring & updates: Stay ahead of the curve

Maintaining accurate records and keeping stakeholders informed is an ongoing process. Borealis CSRD monitoring software helps you stay on top of things with regular updates, efficient metric tracking, and clear communication channels.

Regular updates

- Continuous updates on metrics and target progress.

- Up-to-date record maintenance and stakeholder communication.

Assurance & verification: Build trust and transparency

Having your report verified by a third party adds credibility to your efforts. Borealis CSRD management software provides the tools you need to facilitate this process and ensure the accuracy and completeness of your report, including comprehensive audit trails.

Audit trails

- Comprehensive audit trails for data.

- Facilitates third-party assurance and verification.

- Documents for report accuracy and completeness.

Download the cheat sheet for a quick overview of how Borealis can support CSRD compliance.

Use the CSRD to elevate your digital readiness

It’s estimated that the current digital maturity of many companies is insufficient to meet the CSRD’s demands, which include managing vast amounts of data similar to financial reporting.

Data management maturity involves an organization’s ability to effectively collect, store, manage, analyze and use its data to achieve its business objectives and meet the needs of its stakeholders.

An organization with a high level of data management maturity will have processes, tools and policies in place, including practices such as:

- Data governance

- Data quality

- Data lifecycle management

- Data security

- Advanced analytics

- Advanced Reporting

You don’t have to go it alone – Borealis has been the digital transformation expert for 20 years!

We’ll work with you to create a roadmap that gets you where you need to go, FAST!

Frequently asked questions about CSRD software

What is the CSRD, and what is its purpose?

The CSRD is an EU Directive that amends the scope and the reporting requirements of the Non-Financial Reporting Directive (NFRD). While the NFRD only provided guidelines for ESG reporting, the CSRD will introduce mandatory reporting standards.

Almost 50,000 EU and non-EU companies are expected to report on their sustainability performance under the Corporate Sustainability Reporting. It requires them to present a double materiality assessment of their environmental, social, and governance practices and financial risks within their operations and value chains.

It’s also the first legislation to include the disclosure of targets and forward-looking statements, as opposed to solely historical data.

- The CSRD expands the sustainability reporting requirement to a broader range of companies compared to the previous Non-Financial Reporting Directive (NFRD).

- While the NFRD only applied to companies with more than 500 employees, the CSRD extends to large companies defined as those with over 250 employees €50M turnover, and €25M in total assets.

- Under the CSRD, all listed companies (except micro-enterprises) must report their sustainability performance.

- Non-European companies with branches or subsidiaries in the EU and a net turnover of €150M or more within the EU will also be required to comply with the CSRD, but this requirement will be enforced later.

- With the CSRD, the European Commission defines a common reporting framework for non-financial data for the first time. The Corporate Sustainability Reporting Directive (CSRD) supports investors, consumers, policymakers and other stakeholders in evaluating large companies’ non-financial performance in order to encourage companies to develop more responsible business approaches.

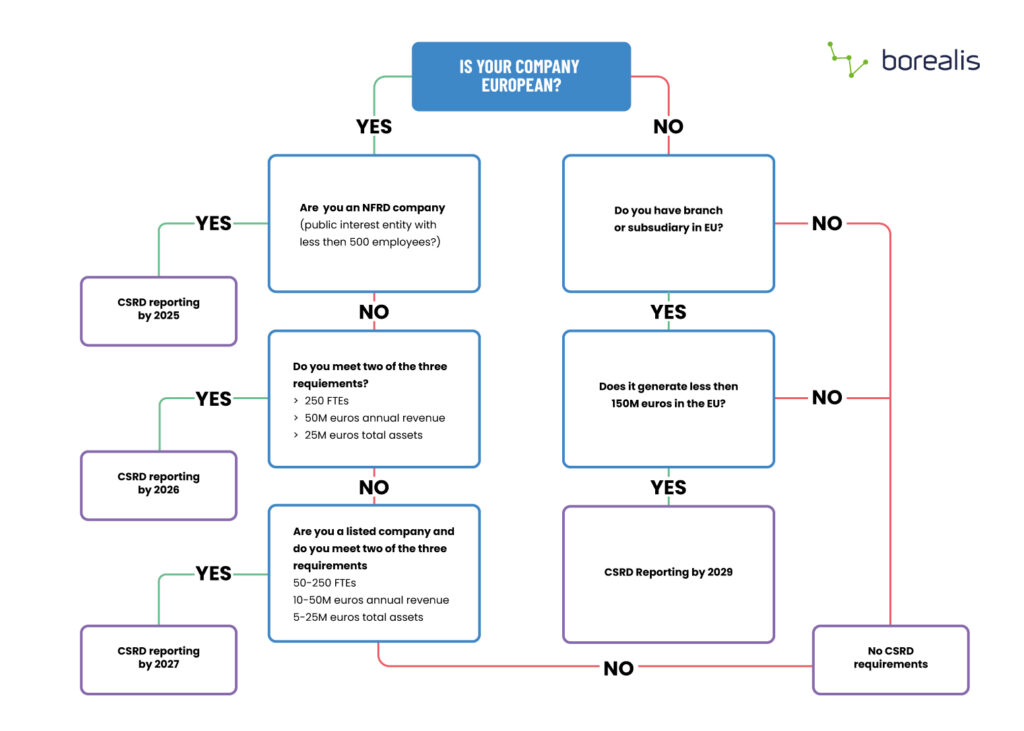

Is there an easy way for companies to determine if they need to report?

YES! We’ve included the following flowchart to help you out.

What’s the timeline for the introduction and reporting around the CSRD?

Phased introduction starts with Public Interest Entities (PIEs) and companies with listed securities on EU-regulated markets with more than 500 employees (e.g. those already subject to reporting requirements under the Non-Financial Reporting Directive).

What are the European Sustainability Reporting Standards (ESRS)?

At the core of the ESRS are the two standards which establish the foundation for CSRD compliance.

ESRS 1: General requirements

These sector-agnostic requirements set general principles for sustainability reporting across various topics. The ESRS 1 also clarifies what information is mandatory, optional, or subject to materiality assessment.

Topics are deemed material for reporting if they are significant from either a risk or an impact perspective. Companies can also include “entity-specific” topics to address their unique industry or circumstances.

For example, Environmental Topics mandate specific disclosure requirements around climate change, pollution, water and marine resources, biodiversity and ecosystems, as well as resource use and circular economy (how well a company has moved away from a linear (take-make-dispose) economy to one where products and materials are reduced, reused, repurposed and recycled.)

Social Topics provide specific disclosure requirements on a company’s own workforce, including governance structures, business strategies, risk management, objectives and organizational information, and disclosures regarding workers in the value chain, plus affected communities, customers and end users.

Governance Topics include:

- Corporate culture

- Supplier relationship management

- Anti-corruption and bribery efforts

- Standards re: political influence and lobbying

- Protection of whistle-blowers

- Animal welfare

- Payment practices

ESRS 2: General disclosures

These requirements specify essential information for preparing a sustainability statement. They mandate information on governance, materiality assessments, key performance indicators, etc. Appendices in the ESRS 2 also list mandatory data points from EU legislation like the Sustainable Finance Disclosure Regulation (SFDR) and the EU Climate Law.

What’s the estimated cost associated with data collection, report preparation and auditing for CSRD?

According to EFRAG (European Financial Reporting Advisory Group), it’s estimated that administrative costs to report for CSRD could range from 0.004% to 0.008% of a company’s yearly revenue, depending on the company’s industry, the information they consider relevant to their investors and other stakeholders, and the maturity of the company’s digital systems for collecting, storing, managing, analyzing and reporting its data.

Related yearly auditing costs for “limited assurance” audits are estimated to range from 0.013% to 0.026% of revenue. The EU rules call for limited-assurance audits to start, with the goal of moving to reasonable assurance in the near future.

How can my company prepare for CSRD compliance?

Initial steps and team coordination

Start by understanding the comprehensive steps required for CSRD reporting and seeking expert support.

Ensure clear communication and alignment among the teams responsible for CSRD reporting, identifying key roles for data collection and sharing. Challenges may include coordinating across departments and establishing clear communication channels. To address this, companies can appoint a dedicated CSRD compliance officer to oversee the process.

Data management strategies

Establish robust mechanisms for data collection, ensuring the data is reliable and standardized. Implement advanced CSRD software solutions to manage and analyze data, enhancing the efficiency of the reporting process.

Organizations may struggle with disparate data sources and inconsistent data quality. Overcoming this requires investing in integrated data management systems and training staff on best practices for data handling. It also means attributing resources to change management in order to ensure tools are being used efficiently.

Legal and reporting framework

Perform a thorough legal entity analysis to determine which entities fall under the CSRD scope. Engage with statutory auditors to align on the reporting framework and understand the nuances of CSRD and its ESRS. The challenge here lies in interpreting complex regulations and ensuring all legal entities comply. Regular consultations with legal experts and auditors can help mitigate these issues.

Leveraging technology for compliance

Adopt a digital-first mindset and invest in cloud-based CSRD software technologies to facilitate integrated financial and ESG reporting. Leverage software solutions to gather and monitor data efficiently.

Beware of shortcuts!

Trying to customize an existing system in place, like a CRM or trying to develop your own solution internally usually ends up being more costly than choosing the right solution in the first place.

Moreover, your chosen CSRD reporting software solution should be scalable, grow with your reporting needs, and provide comprehensive training for your staff to maximize the benefits of these technologies.

How will the CSRD impact businesses?

The Corporate Sustainability Reporting Directive (CSRD) represents a significant change in the way businesses approach sustainability. Beyond a strong regulatory requirement, the CSRD is set to transform operational frameworks, data management practices, and stakeholder engagement strategies.

For businesses to thrive in this new landscape, understanding and adapting to these changes is crucial.

Learn more about Borealis CSRD software and solutions

Contact us

The CSRD necessitates a significant shift in how businesses collect, manage, secure, and report data, and it will require a robust digital-first infrastructure to handle the increased data management challenges.

Find out how Borealis CSRD software can help simplify your CSRD journey by helping with stakeholder engagement, data collection, analysis, reporting, auditing and compliance.